citiesabc, first_page

AI Economy for Europe: The AWS European Sovereign Cloud Case Study

06 Feb 2026

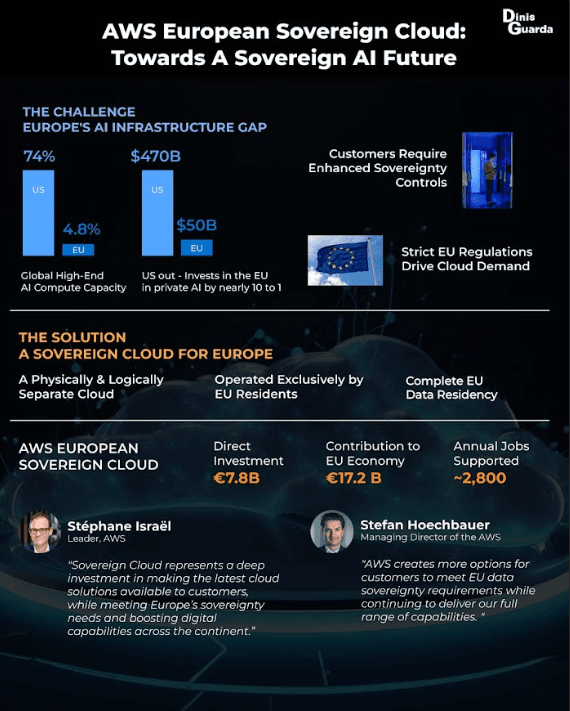

Europe currently owns only a small fraction of global AI compute capacity and hyperscale cloud infrastructure, while most of the capacity and investment is concentrated in the United States and China. At the same time, AI‑driven workloads are projected to more than double global data‑centre electricity consumption by 2030, raising concerns about energy security, water use and environmental sustainability. The new AWS European Sovereign Cloud, designed to operate independently within the European Union and led entirely by EU residents, offers an important opportunity to align these goals and enable an autonomous data and cloud AI economy for Europe

The global digital economy is a multi‐trillion dollar force, projected to surpass $16.5 trillion by the mid-2020s and accounting for nearly one-sixth of total global output. In contrast, the European Union’s digital economy, though steadily expanding, represents a considerably smaller share of both the EU’s own GDP and the global digital landscape.

A similar disparity is evident in the artificial intelligence sector, where Europe accounts for about one-fifth of global AI technology spending, yet attracts only around 10% of private AI investment.

This investment gap highlights a critical need to strengthen the continent’s digital and AI ecosystems.

“AWS offers the most comprehensive and adopted cloud and the AWS European Sovereign Cloud represents a deep investment in making the latest cloud solutions available to customers, while meeting Europe’s sovereignty needs and boosting digital capabilities across the continent.” - Stéphane Israël, Managing Director of the AWS European Sovereign Cloud

Global disparities in AI compute and cloud infrastructure

AI compute dominance and high‑performance computing (HPC)

AI development relies on high‑end compute such as GPU clusters and AI supercomputers. As of May 2025 the United States controlled about three‑quarters of global GPU cluster performance, while China held roughly 15% and traditional HPC leaders in Europe and Japan played marginal roles.

The U.S. also dominated AI supercomputer capacity, with the Federal Reserve noting that the U.S. controlled 74% of global high‑end AI compute, compared with 14% for China and just 4.8% for the EU.

A separate 2025 special report estimated that the U.S. contributed 6.696 exaflops (48.4 %) of Top500 performance and hosted the world’s three exascale machines (El Capitan, Frontier and Aurora), whereas Europe’s total performance was around 1.2 exaflops. While the EU operates advanced machines such as JUPITER, LUMI and Leonardo, these systems provide only a fraction of global AI compute capacity.

JUPITER, inaugurated in September 2025, delivers a full 1 Exaflop performance and uses energy‑efficient warm‑water cooling that can feed heat back into campus heating.

In contrast, China’s publicly reported Top500 performance is just 0.281 exaflops, representing 2% of global public compute; however, officials claim an estimated ≈230 exaflops of national capacity across eight million datacentre racks, illustrating a large pool of unreported “dark compute”.

Hyperscale vs. enterprise data‑centre capacity

Hyperscale data centres—massive facilities operated by major cloud providers—offer far more efficient computing and cooling than smaller enterprise facilities. A Synergy Research Group analysis of Q1 2025 found 1,189 large hyperscale data centres worldwide, accounting for 44% of total data‑centre capacity.

In 2018 on‑premises enterprise facilities accounted for 56% of capacity; by 2025 their share had fallen to 34% and is projected to drop to 20% by 2030. The U.S. hosts more hyperscale capacity than any other region, while Europe lags significantly despite rapid growth in local facilities.

In 2024, the European cloud market reached €61 billion, yet American hyperscalers (AWS, Microsoft and Google) captured 70% of revenues. European cloud providers’ market share dropped from 29% in 2017 to 15% in 2024, even though local providers tripled their revenues over the period.

Investments and AI adoption disparities

Private investment in AI mirrors the compute gap. Between 2013 and 2024, cumulative private AI investment in the U.S. exceeded $470 billion, while the EU attracted roughly $50 billion.

A special report estimated that hyperscale cloud companies were projected to spend ≈$315–320 billion on AI‑ready datacentres in 2025—dwarfing public budgets. This difference has direct implications: high performance compute, research and development (R&D) and talent tend to cluster where investment flows.

European AI adoption levels

Despite the compute deficit, AI adoption in Europe is rising. Eurostat reported that in 2025 around 19.95% of EU enterprises (10+ employees) used at least one AI technology, up from 13.5% in 2024. Adoption varies widely: 55% of large enterprises use AI, compared with 18% of small firms; Denmark and Finland lead with adoption rates above 40%, while countries such as Romania remain below 6%.

This uneven uptake reflects the complexity of AI deployment, limited compute access and concerns about data security and sovereignty. In a McKinsey survey, 44% of technology leaders cited data‑security concerns and 31% cited data‑residency requirements as barriers to cloud adoption in Europe.

Environmental and infrastructure challenges

Energy consumption and grid constraints

AI workloads dramatically increase data‑centre energy demand. The International Energy Agency (IEA) estimates that global data‑centre electricity consumption was 415 terawatt‑hours (TWh) in 2024, roughly 1.5% of world electricity use. Consumption has grown 12% annually since 2017 and is projected to more than double to 945 TWh by 2030. The United States accounted for about 45% of this consumption in 2024, China 25% and Europe 15%. The IEA warns that data‑centre demand could represent 5–10% of peak electricity load in large European countries if all planned facilities are built, but connecting these centres to congested grids can take seven to ten years. Data centres are expected to account for around 10% of EU electricity demand growth by 2030.

Cooling and water use

Cooling is the dominant overhead in data‑centre operation. The IEA reports that hyperscale data centres can achieve power usage effectiveness (PUE) around 1.15, meaning only 0.15 kWh is consumed for cooling and auxiliary loads for every 1 kWh of IT power, whereas enterprise facilities often have PUE near 2. Public reporting from AWS reveals that its global data centres achieved a PUE of 1.15 in 2023, with the most efficient European site reaching 1.04. Google’s cloud region is slightly lower at 1.10. Most enterprise on‑premises facilities operate at PUE ≈ 1.8—implying large energy and cost savings for organisations migrating to hyperscale cloud.

Water consumption adds another dimension. The Environmental and Energy Study Institute notes that a medium‑sized data centre can use up to 110 million gallons of water annually, equivalent to the consumption of 1,000 households, while large facilities may use up to 5 million gallons per day. U.S. data centres collectively consumed 449 million gallons of water per day in 2021. Each 100‑word AI prompt may indirectly use about 519 ml of water for cooling. Closed‑loop and immersion cooling technologies can reduce freshwater use by up to 70%, while warm‑water systems such as the one in Europe’s JUPITER supercomputer recover waste heat for local heating. Efficient cooling therefore plays a crucial role in sustainable AI deployment.

Europe’s digital strategy and human‑centric AI policy

Digital Decade and cloud targets

The European Commission’s Digital Decade programme aims for 75% of EU businesses to use cloud‑edge technologies by 2030, and for 10,000 climate‑neutral edge nodes to be deployed. As of 2025, 45.2% of EU businesses (77.6% of large firms) use cloud services. To achieve these targets, the Commission plans to triple EU data‑centre capacity within 5–7 years under the forthcoming Cloud and AI Development Act and to develop an EU‑wide cloud policy and certification scheme emphasising energy efficiency and security.

Human‑centric AI and regulatory frameworks

Europe’s approach to AI is rooted in human rights, fairness, transparency and sustainability. The European Union’s Human‑Centric AI framework emphasises a risk‑based legal approach (as enshrined in the AI Act, adopted in 2024), promoting technical robustness, human agency, privacy and non‑discrimination. The framework calls for AI systems to improve human welfare and prioritises human flourishing over mere economic success. The Commission invests €1 billion annually via Horizon Europe and Digital Europe, with a plan to mobilise €20 billion per year in combined public‑private investment to boost AI adoption. The AI Continent Action Plan (April 2025) aims to develop large‑scale AI data and computing infrastructures while ensuring democratic values are upheld. Policy coordination also extends to data governance: the Human‑Centric Roadmap for Europe proposes market incentives (tax and procurement advantages) for organisations adopting ethical, user‑centric data practices and calls for hybrid cloud‑edge sovereignty so individuals retain control over their data. Such measures highlight that digital sovereignty is not just about geographic storage, but also about operational control, trust, and democratic oversight.

Energy and grid integration

Multiple European policy and research bodies warn that electricity infrastructure is the major bottleneck for AI and cloud growth. The CERRE research report notes that to maintain competitiveness, Europe must streamline permitting, incentivise 50–60 GW of demand‑side flexibility by 2035, integrate data centres into spatial and electricity planning, and publish transparent PUE metrics. Without coordinated planning, grid connection delays of up to 10 years and local congestion threaten to stall data‑centre projects. To support sustainability and sovereignty simultaneously, data centres should be sited near abundant renewable energy sources and use heat recovery to support local communities.

The need for cloud and AI sovereignty

Global sovereign cloud market and drivers

The global sovereign cloud market is projected to exceed $250 billion within three years. Gartner expects 75% of enterprises outside the United States to implement digital sovereignty strategies by 2030. Leaders increasingly recognise that AI, crypto and sovereign debt bubbles all depend on concentrated cloud infrastructure; more than two‑thirds of global cloud infrastructure spending is controlled by a few hyperscalers. A World Economic Forum analysis warns that this concentration, combined with financial bubbles and geopolitical tension, creates systemic risk. 61% of CIOs in Western Europe now say geopolitical risks will restrict their use of global cloud providers. Consequently, Europe’s new Cloud Sovereignty Framework ties sovereignty requirements directly to procurement, compelling vendors to demonstrate operational control rather than merely data‑residency claims.

European cloud market dynamics and sovereignty concerns

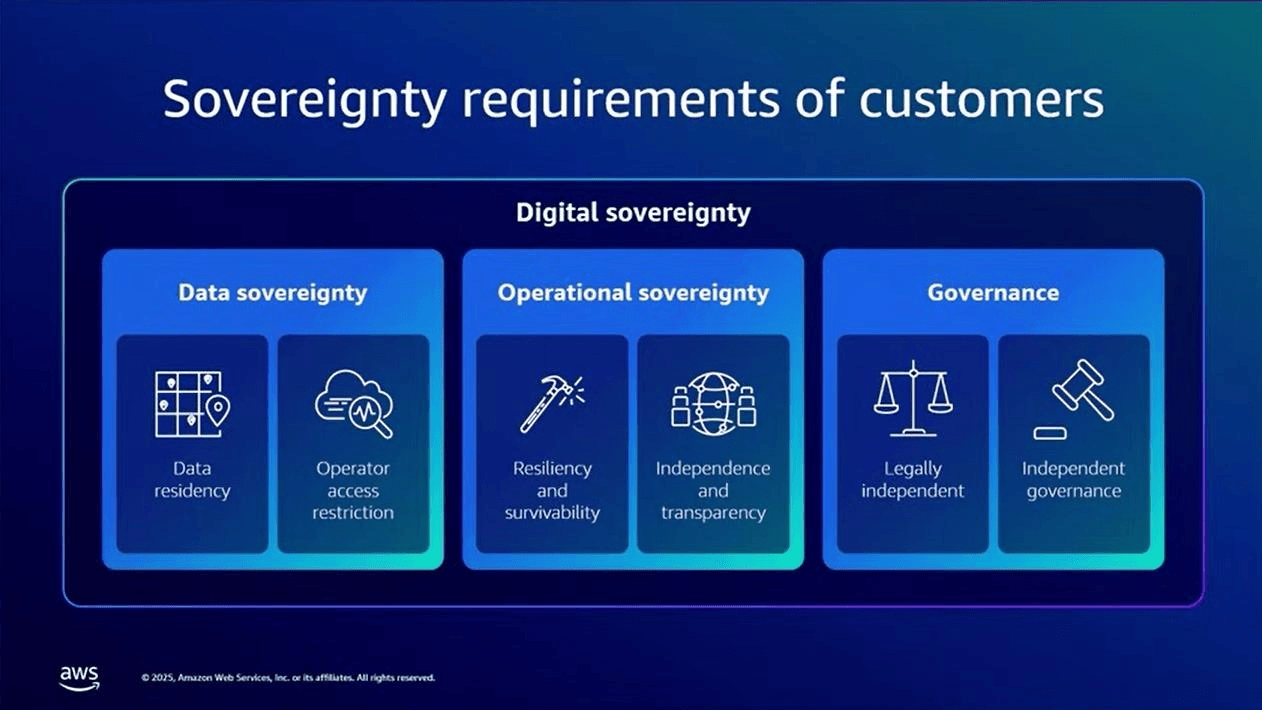

European policymakers worry that up to 90% of European data resides outside EU‑controlled infrastructure, and that global hyperscalers provide 72% of cloud services in Europe. Data volumes are projected to balloon from 33 zettabytes in 2018 to 572 zettabytes by 2030, intensifying sovereignty concerns. IDC predicts global spending on sovereign cloud solutions will reach USD $258.5 billion by 2027. Observers note that U.S. laws such as the Cloud Act allow government access to data stored abroad by American companies, undermining trust in trans‑Atlantic data handling. A Vodafone analysis argues that sovereignty encompasses data, operational and technological dimensions, and emphasises risk‑based approaches rather than strict exclusion of foreign providers; partnerships with trusted operators are needed because building a competitive European hyperscaler from scratch is unrealistic. The optimum solution is selective interdependence: ensure Europe retains control over sensitive workloads while leveraging global innovation..

AWS European Sovereign Cloud—governance and features

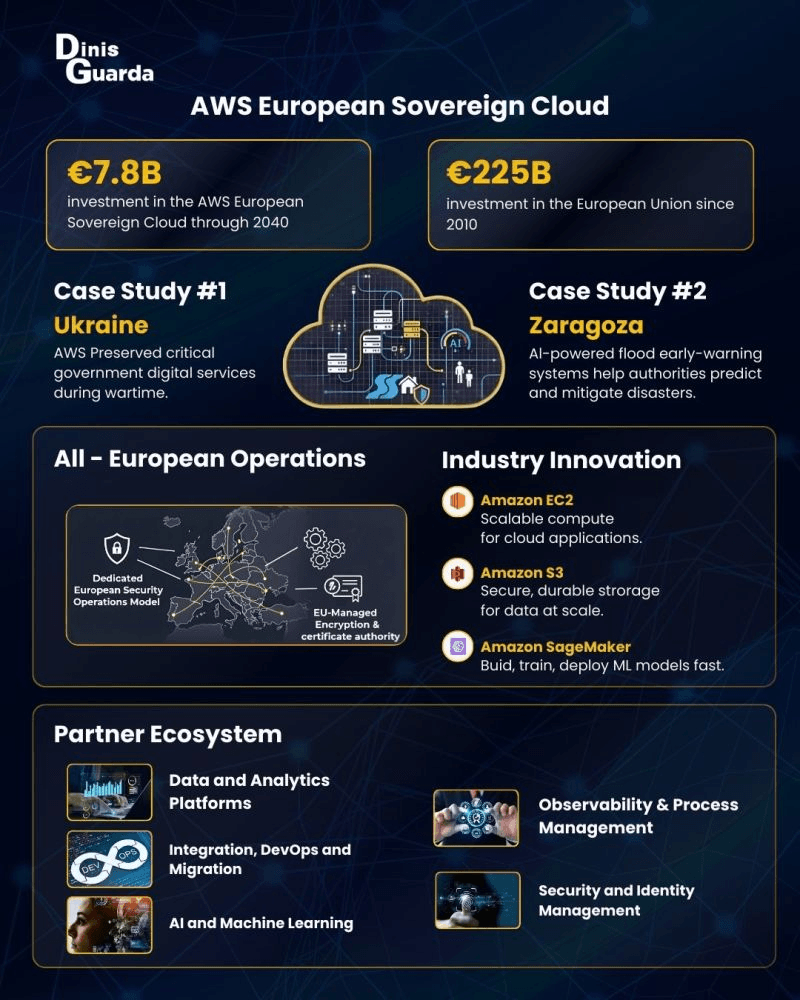

AWS has designed a sovereign cloud infrastructure tailored to Europe’s needs. According to Amazon, the AWS European Sovereign Cloud will operate entirely within the EU and be physically and logically separate from other AWS regions. Its parent company and three subsidiaries will be incorporated in Germany, led by EU citizens and subject to local laws.

"At Amazon Web Services (AWS) we are proud of what the European Sovereign Cloud represents. It creates more options for customers to meet EU data sovereignty requirements while continuing to deliver our full range of capabilities. " - Stefan Hoechbauer, Managing Director of the AWS European Sovereign Cloud

The management team—including the managing director, security and privacy officials—must all be EU residents. An independent advisory board composed of four EU citizens will provide accountability on sovereignty issues and ensure the cloud can operate independently even in the event of global connectivity disruptions. Key characteristics include:

- Operational autonomy: The cloud will have no critical dependencies on non‑EU infrastructure. All control systems, root certificates and trust services will be held within the EU, and only EU‑resident AWS employees will operate the services. Authorised EU‑based employees will maintain an independent replica of the source code to ensure continuity during disruptions.

- Full‑featured services: Customers will access the same AWS services (including AI/ML, advanced compute, storage, and networking) and security innovations such as the AWS Nitro System. Unlike many sovereign offerings that strip capabilities to meet compliance, AWS promises feature parity with its global cloud.

- Data‑residency and compliance: Dedicated European subsidiaries will keep customer content and metadata within the EU. Bills and consoles will be provided in Euro, and the service is designed to meet stringent regulatory, data‑residency and operational needs.

- Resilience and security: Independent operations across multiple Availability Zones will provide high availability; if connectivity to the global AWS network is lost, services can continue indefinitely. A dedicated EU Security Operations Center will oversee operations.

- European leadership: The first managing director, Kathrin Renz—a German national—will lead the organisation and act as the most senior decision‑maker.

The cloud features multiple Availability Zones with independent power, networking, and security capabilities, ensuring that critical operations, such as energy management and emergency response, remain functional even during extreme events like natural disasters.

For example, AWS’s support for Ukrainian government services during the ongoing crisis highlights the importance of having a resilient infrastructure that can continue functioning despite significant disruptions.

Similarly, AWS’s work in Zaragoza, where it developed AI-powered flood prevention systems, demonstrates the ability of cloud technology to drive sustainable urban solutions in times of crisis. Such systems help cities monitor and mitigate risks associated with extreme weather events, contributing to climate resilience in urban areas.

In addition to operational resilience, the AWS European Sovereign Cloud is designed to support sustainability initiatives. The cloud’s architecture allows for optimised resource usage, ensuring that energy-efficient operations are central to its design. This capability aligns with Europe’s green agenda, which aims to reduce carbon emissions and enhance environmental sustainability.

AWS’s European Sovereign Cloud will support the full suite of AI services, such as Amazon SageMaker, Amazon Bedrock, and Amazon Q, giving cities the tools they need to integrate machine learning models, predictive analytics, and automation into their operations.

Implications for businesses and investors in the EU

Meeting regulatory requirements

For organisations in regulated sectors such as healthcare, finance, public administration and defence, compliance with EU laws (GDPR, AI Act, eIDAS) is non‑negotiable. The AWS European Sovereign Cloud offers a robust solution that addresses data‑residency, encryption and operational control requirements. With an independent governance structure and EU‑resident operators, businesses can minimise exposure to extraterritorial requests (e.g., the U.S. Cloud Act) and reassure regulators and customers that data is protected. EU‑based billing and currency support simplify financial management. Investors should recognise that compliance frameworks drive adoption: Gartner expects that sovereign cloud strategies will become mainstream by 2030, and IDC predicts sovereign cloud spending will surpass $258 billion by 2027.

Reducing risk and enhancing resilience

Geopolitical tensions and cybersecurity risks pose significant threats to businesses using globally distributed cloud services. The AWS sovereign cloud’s ability to operate independently of the global network and to continue running during connectivity interruptions reduces operational risk. Dedicated EU‑based security operations and separate control plane mitigate the risk of cross‑border legal compulsion. For investors, this reduces regulatory uncertainty and potential compliance liabilities, making European workloads more predictable.

Accelerating AI innovation and productivity

European businesses currently face compute bottlenecks and limited access to large‑scale AI infrastructure. McKinsey estimates that a high‑sovereignty AI scenario could unlock up to €480 billion in annual value for Europe by 2030, comprising €63 billion GDP uplift for AI makers and €416 billion from productivity gains for AI takers. Access to a sovereign, full‑featured cloud allows organisations to build and deploy large language models, run high‑performance simulations and adopt generative AI tools without moving data outside the EU. SMEs and start‑ups in areas such as manufacturing, healthcare, finance and education can tap into high‑end compute, levelling the playing field with U.S. and Chinese competitors. EuroHPC’s exascale systems (JUPITER, LUMI, Leonardo) will complement sovereign cloud offerings for research and training workloads.

Sustainability and cost efficiency

Hyperscale providers like AWS operate with lower PUE (≈ 1.15) compared with typical on‑premises data centres (≈ 1.8). Migrating workloads to energy‑efficient sovereign cloud regions can reduce electricity consumption by up to 30–50 % and facilitate the use of renewable energy through power purchase agreements. Warm‑water cooling and heat recovery, as used by Europe’s JUPITER supercomputer, demonstrate how data centres can serve as district heating sources, turning infrastructure into a civic asset. Investors should note that energy‑efficient operations not only reduce operational costs but also align with ESG requirements and forthcoming EU energy‑efficiency directives.

Supporting cross‑border collaboration and data union initiatives

The EU’s Human‑Centric Roadmap emphasises hybrid cloud‑edge sovereignty and values‑based partnerships. Sovereign cloud infrastructure can support cross‑border research projects, AI factories and data‑union initiatives by providing trusted environments for data sharing. By embedding human‑centric safeguards into procurement and partnership models, organisations can build ecosystems that respect privacy while unlocking value. Start‑ups and SMEs should explore programmes such as JUPITER AI Factory and regional AI factories that offer access to exascale supercomputers and tailored support.

Recommendations for policymakers, businesses and investors

- Strategic infrastructure investment: Policymakers should fast‑track permitting, grid integration and renewable energy projects to ensure that sovereign cloud regions can connect to low‑carbon power sources. Supporting research into immersion and warm‑water cooling technologies can reduce water use and recover waste heat.

- Balanced digital sovereignty: Adopting sovereign cloud does not mean isolating Europe from global innovation. A risk‑based approach—hosting sensitive workloads on sovereign cloud while leveraging global cloud for non‑critical functions—can maximise flexibility. Public‑private partnerships with trusted hyperscalers can accelerate the build‑out of sovereign capabilities.

- Support for SMEs and AI adoption: Governments and investors should provide grants, vouchers and technical assistance to help small and medium‑sized enterprises adopt AI services on sovereign cloud. Eurostat data show that large enterprises dominate AI adoption; targeted programmes can close this gap and ensure inclusive growth.

- Transparent metrics and standards: Regulators should require data‑centre operators to disclose PUE, water usage effectiveness (WUE) and carbon intensity. Harmonised standards across the EU will allow investors and customers to compare providers and drive competition towards efficiency and sustainability.

- Human‑centric design and ethical governance: Businesses should incorporate the EU’s ethical guidelines—human agency, fairness, transparency and sustainability—into AI development. Sovereign clouds must support privacy‑enhancing technologies, accountability mechanisms and open‑source models to build public trust.

- Long‑term talent and R&D investment: Europe needs to build a skilled workforce to operate and innovate on sovereign cloud platforms. Investments in AI education, research partnerships and cross‑disciplinary programmes are essential to reduce dependence on external talent and accelerate the development of indigenous AI solutions.

Conclusion

The launch of the AWS European Sovereign Cloud marks a pivotal moment for Europe’s digital and AI landscape. It directly addresses the continent’s compute deficit, sovereignty concerns and environmental challenges while aligning with the EU’s human‑centric values and regulatory framework. By offering operational autonomy, full‑featured services, EU‑resident control and energy‑efficient infrastructure, AWS’s sovereign cloud can catalyse a human‑centric AI economy that balances innovation with trust, sustainability and democratic oversight. Businesses and investors in the EU region should view sovereign cloud adoption not as an optional compliance exercise, but as a strategic enabler of competitive advantage, resilience and long‑term value creation.