citiesabc, first_page

India Data Center Market: Comprehensive Analysis and Investment Outlook (Part 2)

Industry Expert & Contributor

04 Feb 2026

Capital Influx

Between 2020 and 2025, more than USD 14 billion has been invested in India's data center sector, while announced pipeline commitments exceed USD 20 billion, highlighting the sector's resilience amid global macroeconomic challenges. If realised, these substantial capital commitments could increase India's current data center capacity by 35 to 40 percent, positioning the country as a potential regional hub for AI infrastructure.

Growth is primarily driven by global hyperscalers, supported by infrastructure asset status that facilitates longer-term financing, reduced capital costs, and faster regulatory approvals. Large conglomerates such as Adani are expanding rapidly through integrated models that combine data centers, power, and real estate, thereby reducing execution risk. Colocation operators are also expanding, with strategic investments in Tier-2 and non-metropolitan cities that benefit from lower costs and state-provided incentives.

Deal-wise Investment Summary: India Data Centre Market

| Investor / Operator | Investment Size (USD) | Planned Capacity / Scope | Primary Location(s) | Strategic Rationale / Notes |

|---|---|---|---|---|

| Reliance Industries | ~USD 30 billion | ~3 GW AI & DC campus | Jamnagar, Gujarat | Largest single DC commitment in India; positions India as a regional AI & compute hub |

| AWS (Amazon Web Services) | Part of USD 15+ billion (with peers) | Multi-phase hyperscale capacity | Mumbai, Chennai, Hyderabad | Cloud expansion aligned with enterprise & AI demand |

| Microsoft Azure | Part of USD 15+ billion | Hyperscale DC regions | Mumbai, Hyderabad | Focus on cloud, AI, and enterprise workloads |

| Google Cloud | Part of USD 15+ billion | Hyperscale & ecosystem investments | Mumbai, Chennai | Reinforced by AdaniConneX JV |

| Adani Group (Standalone) | ~USD 10 billion | Multi-city DC expansion | Mumbai, Chennai, Hyderabad | Leverages integrated power, land, and infra capabilities |

| AdaniConneX (Adani–Google JV) | Up to USD 15 billion (ecosystem) | DCs + power + connectivity | Pan-India | Vertically integrated DC + renewable + connectivity model |

| STT GDC India | ~USD 3.2 billion | Expansion of colocation footprint | Mumbai, Chennai, NCR, BLR | Hyperscale-led demand, long-term contracts |

| CtrlS Datacenters | ~USD 2 billion | Multi-campus expansion | Hyderabad, Mumbai, Chennai | Strong enterprise & government client base |

| NTT Global Data Centers | ~USD 1.5 billion | Doubling India capacity | Mumbai, Chennai, BLR | Global hyperscale and enterprise strategy |

| Yotta Infrastructure | ~USD 1–1.2 billion (announced) | NM1–NM2 hyperscale campuses | Navi Mumbai | Focus on scalable hyperscale platforms |

| RackBank | USD 120 million (Phase 1) → USD 360 million (total) | 80 MW AI-focused facility | Raipur, Chhattisgarh | First hyperscale-grade DC in central India; Tier-2 strategy |

| Web Werks / Iron Mountain | ~USD 1 billion+ (combined pipeline) | Colocation & hyperscale | Mumbai, Chennai | JV-led expansion, enterprise focus |

Infrastructure Constraints and Resource Limitations

India's data center growth depends more on the availability and coordination of key infrastructure than on demand. Factors like power, water, land, capital and clear policies shape how quickly and where new capacity is added.

Infrastructure Limitations Impacting India's Data Center Market

| Constraint Area | Structural Challenge | Market Impact | Mitigation Pathways |

|---|---|---|---|

| Power Availability & Grid Capacity | Limited access to reliable, scalable power; grid congestion in Tier-1 metros; long timelines for high-voltage connectivity | Delayed project commissioning, higher operating costs, constraints on AI-grade high-density deployments | Dedicated data-center power corridors, open-access renewable procurement, captive generation with storage, coordinated grid planning |

| Water Availability & Cooling Resources | High water intensity of conventional cooling; stress in water-scarce urban regions; limited treated water infrastructure | Approval delays, sustainability risks, rising operational costs, community resistance | Shift to liquid and closed-loop cooling, use of treated/recycled water, water-positive facility design |

| Sustainability vs. Scale Trade-off | Rapid capacity expansion conflicts with energy and water sustainability objectives, especially for AI workloads | ESG risk exposure, increased regulatory scrutiny, investor pressure on hyperscale operators | Renewable PPAs, stricter PUE/WUE benchmarks, ESG-linked financing, efficiency-first design |

| AI-Ready Compute Infrastructure | India generates ~20% of global data but hosts ~3% of global data center capacity; limited GPU-dense facilities | Risk of AI workload migration offshore; slower domestic AI ecosystem development | Incentives for AI-optimised data centers, GPU clusters, high-density campus zoning |

| Capital Intensity | High upfront investment (INR 60–70 crore per MW) including power and cooling infrastructure | Slower scaling, higher entry barriers, increased reliance on foreign capital | Infrastructure status, long-tenor debt access, REITs, public–private partnership models |

| Land Availability & Urban Concentration | Scarcity and high cost of land in Tier-1 metros; zoning and permitting complexity | Cost inflation, execution delays, geographic concentration risk | Data-center parks, industrial corridors, satellite campuses outside core metros |

| Policy Fragmentation | Variability in state-level incentives, power tariffs, water access policies, and approvals | Regulatory uncertainty, uneven capacity distribution across states | Harmonised national data center and AI infrastructure policy with state alignment |

| Tier-2 & Tier-3 Infrastructure Gaps | Power redundancy, fiber depth, and water recycling infrastructure still evolving | Slower hyperscale adoption despite cost advantages | Phased development, edge-first deployments, public investment in utilities |

| Tier-2 & Tier-3 Structural Advantages | Lower land and water costs; faster approvals; proximity to regional demand | Enables cost-efficient expansion, edge computing, disaster recovery capacity | Position Tier-2/3 cities as edge, inference, and overflow hubs |

Research Insight: Multiple studies consistently indicate that India's data center growth is limited primarily by infrastructure readiness and resource coordination, rather than by demand. Power and water availability are becoming critical constraints, especially for facilities focused on artificial intelligence. However, Tier-2 and Tier-3 cities present structural advantages, provided that targeted investments in utilities, connectivity, and policy harmonisation are implemented.

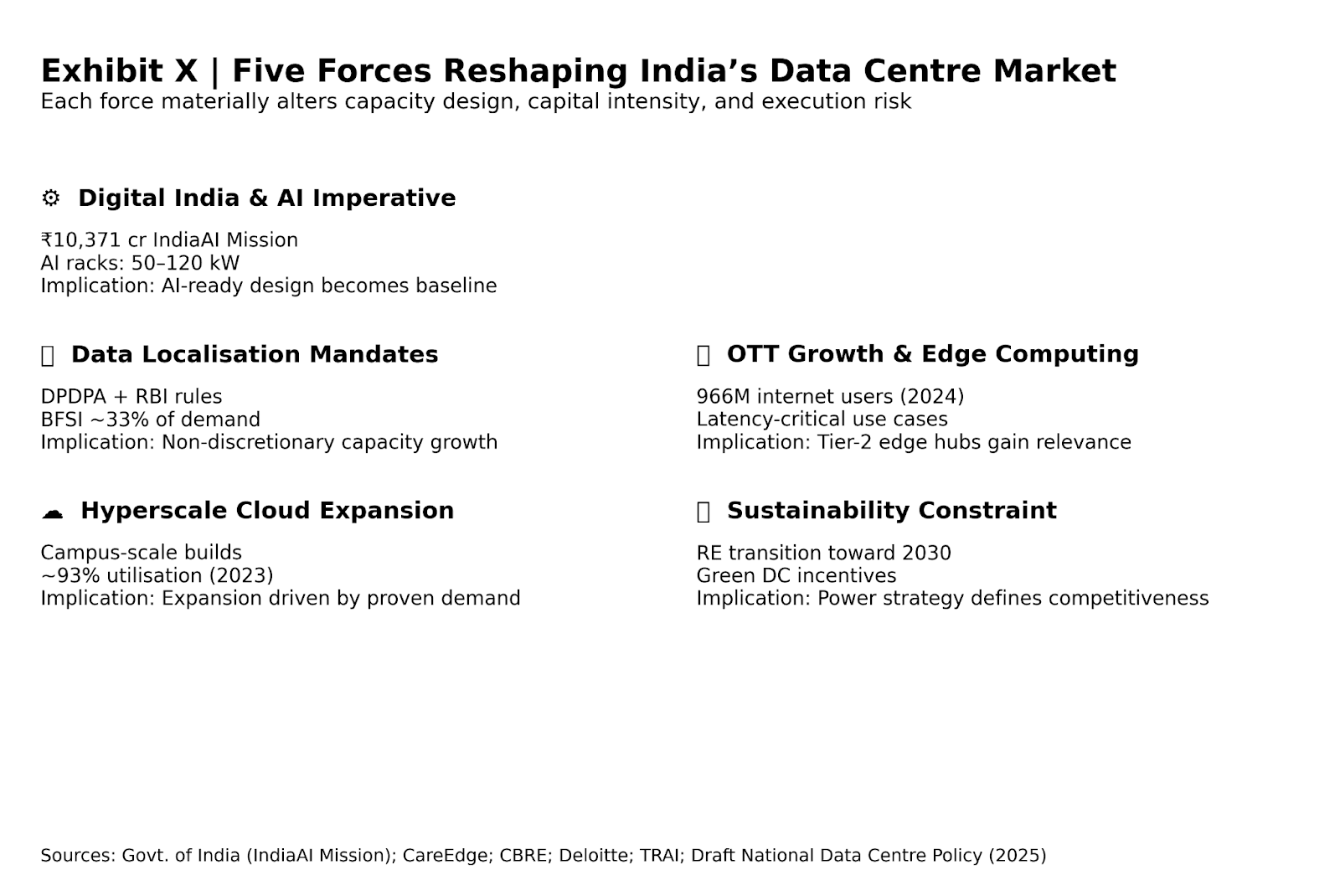

Five Forces Reshaping the Market

The Indian data center market is now primarily influenced by AI intensity, regulatory requirements, hyperscale economics, network decentralisation, and sustainability constraints, rather than by general digital growth. The interplay among these factors is accelerating market expansion and raising operational thresholds, thereby favouring operators with access to capital, reliable power, and policy alignment.

1. Digital India & the AI Imperative

Recent digital policy in India designates computing infrastructure as essential national infrastructure. Through the IndiaAI Mission, the government has allocated ₹10,371 crore (approximately USD 1.25 billion) to acquire 10,000 GPUs, highlighting the critical importance of AI capacity in public services, education, healthcare, and financial inclusion.

AI workloads are significantly transforming data center economics, with rack densities increasing from 5–10 kW (traditional enterprise) to 50–120 kW per rack for AI training and inference. Industry consensus indicates that AI-related workloads could comprise approximately 50% of total data center capacity within the next decade. This shift necessitates that operators redesign power, cooling, and facility layouts, and increases the risk of obsolescence for assets not configured for AI workloads.

2. Data Localisation as Non-Discretionary Demand

India's data localisation framework has established regulatory compliance as a structural driver of demand. The Digital Personal Data Protection Act (DPDPA) and sector-specific mandates, particularly those issued by the Reserve Bank of India, require the domestic storage and processing of sensitive data across sectors such as BFSI, government, telecom, and healthcare.

The BFSI sector alone accounts for approximately 33% of data center end-user demand, underscoring the necessity for compliance-driven capacity expansion. Foreign cloud providers that previously served Indian demand from offshore locations are now required to procure or develop domestic capacity, resulting in sustained, policy-driven demand that is less sensitive to economic cycles.

3. Hyperscale Cloud Platform Expansion

Hyperscale cloud providers are shifting from incremental expansions to campus-scale, platform-level deployments, capitalising on India's coastal connectivity advantages. Mumbai and Chennai serve as international data gateways, supported by 17 subsea cables and 14 landing stations, enabling high-capacity, low-latency global connectivity.

Market fundamentals support continued expansion: capacity utilisation increased from approximately 82% in 2019 to 93% in 2023, while operator revenues grew at a compound annual growth rate of 25% from FY2017 to FY2023, with further acceleration expected. As a result, capacity additions are now driven by utilisation rather than speculation, reinforcing long-term market confidence.

4. OTT Growth and Edge Computing

India's evolving digital consumption patterns are driving a shift toward distributed infrastructure. With 966 million internet connections as of June 2024 and increasing rural broadband adoption, latency-sensitive applications are expanding beyond Tier-1 metropolitan areas.

While OTT streaming can tolerate moderate latency, applications such as interactive gaming, telemedicine, and real-time analytics require near-instant response times. This demand is prompting the deployment of edge data centers in Tier-2 cities, including Pune, Jaipur, Kochi, and Bhubaneswar, creating a hub-and-spoke architecture that supplements rather than replaces hyperscale metropolitan centers.

5. Sustainability as an Operational Constraint

Sustainability has evolved from a reputational concern to a core operational parameter. Hyperscale and enterprise customers increasingly require colocation partners to meet renewable energy and carbon-efficiency thresholds in their procurement decisions.

Leading operators have publicly committed to achieving 100% renewable energy by 2030, supported by long-term power purchase agreements, on-site solar installations, and grid-scale renewable partnerships. Policy alignment reinforces this shift, as the Draft National Data Center Policy (2025) proposes fiscal incentives for green-certified facilities, thereby integrating sustainability directly into project economics.

Strategic Outlook: Navigating Opportunity and Risk

Structural Opportunity

India's data center growth is driven by structural, non-cyclical demand factors. Regulatory mandates under the Digital Personal Data Protection Act (DPDPA) formalise domestic infrastructure requirements, particularly in the banking, financial services, and insurance (BFSI) sector, which accounts for about 32% of end-user demand.

India maintains a cost advantage, with development costs near USD 7 per watt and electricity tariffs roughly 20% lower than those in the United States, supporting global competitiveness. These fundamentals are further strengthened by infrastructure status, state-level incentives, and India's emergence as a regional connectivity hub through extensive subsea cable infrastructure.

Demand Diversification and Digital Expansion

Demand is becoming more multi-sectoral and geographically distributed, which reduces exposure to sector-specific downturns. Increases in over-the-top (OTT) media consumption, digital payments, e-commerce, and government digitalisation are complemented by the rapid adoption of artificial intelligence (AI) across sectors such as healthcare and agriculture.

With approximately 966 million internet connections and growing rural penetration, India's digital expansion supports sustained utilisation of both hyperscale and edge data center infrastructure. This diversity enhances demand resilience and promotes long-term asset utilisation.

Key Risks and Constraints

Execution risks are significant. Grid reliability varies widely across regions, making site selection and power redundancy critical to project viability. Water scarcity in major development zones presents an increasing operational constraint, exacerbated by climate variability.

Global supply-chain constraints for graphics processing units (GPUs), power electronics, and advanced cooling systems introduce schedule and cost risks. Additionally, shortages of specialised operational talent limit the potential for scale-up, despite a broad base of engineering talent. Regulatory risk stems from state-level policy divergence and evolving national compliance requirements, creating uncertainty for long-term planning.

Strategic Imperatives for Operators

From an innovation and operational perspective, long-term renewable power purchase agreements (PPAs), advanced cooling systems such as liquid or hybrid solutions, and modular, scalable design have become essential. Geographic diversification across Tier-1 and Tier-2 locations reduces concentration risk and supports the deployment of edge architectures.

Sustainability certifications, including Leadership in Energy and Environmental Design (LEED) and Indian Green Building Council (IGBC) standards, are shifting from differentiators to baseline procurement requirements, reflecting increased client-driven environmental, social, and governance (ESG) scrutiny. Firms that integrate power, cooling, and connectivity strategies achieve lower lifecycle costs and create higher switching barriers.

Implications for Stakeholders

- Investors should prioritise locations with proven grid reliability and water resilience, and assess state incentives alongside power and water economics. Forming joint ventures with local operators can significantly reduce regulatory and execution risks.

- Enterprise users should align Tier certification with workload criticality, verify renewable energy sourcing and data sovereignty compliance through third-party audits, and implement multi-region disaster recovery as a standard practice.

- Technology vendors are experiencing increased demand for liquid cooling, energy optimisation with power usage effectiveness (PUE) of 1.3 or lower, water recycling, and artificial intelligence-driven data center infrastructure management (DCIM) systems. Innovation is becoming the primary driver of growth in this sector.