citiesabc, first_page

India’s Data Center (Part 3/4): Technological Transformation & Economy

Industry Expert & Contributor

16 Feb 2026

What challenges is India facing when it comes to AI and high-performance computing? Can India’s cooling, power, and water systems scale sustainably enough to support an AI-driven future without creating new national infrastructure bottlenecks? This is the third article from the India’s Data Center series, a research work done in collaboration with Dinis Guarda, and our Citiesabc team.

India’s data centre sector is entering a structural reset. What was once an exercise in capacity addition, more land, more power, more racks, is now being reshaped by physics, infrastructure limits, and long-term sustainability economics.

Artificial intelligence workloads are redefining compute intensity, pushing rack densities far beyond what conventional air-cooled, grid-dependent facilities were designed to handle. At the same time, rising scrutiny on energy use, water consumption, and carbon intensity is turning operational efficiency from a cost consideration into a strategic determinant of competitiveness.

This transformation is exposing a critical reality: data centres are no longer passive consumers of power and water, but active participants in India’s energy and resource systems. Cooling architecture, power sourcing, storage, and water reuse are converging into a single engineering problem. Decisions around liquid cooling, low-PUE design, firm renewable power, and circular water management now influence site selection, capital allocation, and long-term viability as much as demand projections or connectivity.

The defining question is can India engineer an AI-ready digital infrastructure that is reliable, resource-efficient, and sustainable under real-world constraints?

Let’s find out.

Innovations in Cooling, Power, and Resource Management

The increasing rack densities resulting from artificial intelligence and high-performance computing workloads are fundamentally altering data center engineering requirements. Traditional air-cooling systems, originally designed for rack densities of 5 to 10 kW, are nearing their operational limits as AI workloads frequently surpass 50 to 100 kW per rack.

The Shift to Liquid Cooling

Due to air's low heat capacity, its effectiveness diminishes at higher densities, necessitating a shift to liquid-based cooling solutions such as direct-to-chip cold plates and immersion cooling. Empirical research and initial production deployments demonstrate that liquid cooling can achieve approximately 25 to 35 percent improvements in energy efficiency compared to conventional air systems, while also supporting significantly greater compute density per unit area.

Production environments now utilise liquid cooling systems capable of supporting over 100 kW per rack, and facilities optimised for AI workloads are achieving Power Usage Effectiveness (PUE) values close to 1.3. This performance significantly surpasses the global data center average of 1.5 to 1.8. A PUE of 1.3 indicates that only 0.3 kW of auxiliary power is required per 1 kW of IT load, underscoring the value of integrated cooling design over retrofitting existing systems.

Power Infrastructure Challenges

Power infrastructure presents a significant systemic constraint. Although data centers currently consume less than 0.5 percent of India's total electricity, anticipated expansion will result in a disproportionate increase in grid dependency. Mission-critical digital infrastructure requires reliability standards exceeding 99.999 percent uptime, a benchmark not consistently met by many regional grids.

As a result, operators maintain redundant backup systems, traditionally diesel-based, which introduce both economic and environmental challenges despite increased renewable energy procurement. As installed capacity approaches multi-gigawatt levels, power sourcing, redundancy strategies, and grid integration are emerging as strategic differentiators.

Power Infrastructure Metrics

Metric | Value / Estimate | Primary Constraint / Implication |

| Current electricity consumption (2024) | <0.5% of national electricity generation | Indicates near-term headroom, but masks localised grid stress and reliability gaps |

| Grid reliability requirement | ≥99.999% uptime (“five nines”) | Regional grids do not consistently meet mission-critical reliability standards, necessitating redundant backup systems |

| Projected electricity share (2026) | ~2% of national electricity demand | Grid adequacy becomes location-specific; reliability and evacuation capacity emerge as gating factors |

| Regional reliability outlook (2026) | Uneven “five nines” capability across states | Metro and coastal hubs advantaged; inland and Tier-2 regions face higher execution risk |

| Projected electricity share (2030) | ~8% of national electricity demand (~17 GW IT capacity) | Power sourcing transitions from operational issue to strategic national infrastructure question |

| Power sourcing challenge (2030) | Firm, 24×7 low-carbon supply at scale | Renewable intermittency, storage availability, and transmission capacity become binding constraints |

| Development cost per MW | INR 60–70 crore (USD 7.2–8.4 million) | Rising land prices, AI-ready power and cooling equipment, and grid-connection costs inflate capex |

| Cost structure sensitivity | High exposure to power tariffs and state policies | Inter-state tariff differentials materially influence site selection and long-term operating economics |

Water Consumption and Management

Water consumption constitutes an additional resource constraint. Evaporative cooling systems may require up to 25 million liters of water per megawatt annually, which raises sustainability concerns in water-scarce urban areas.

Research and green-building standards increasingly prioritise Water Usage Effectiveness (WUE) metrics, with certification programs promoting benchmarks below 2.2 liters per kWh. Mandatory water impact assessments in major metropolitan areas, along with the implementation of rainwater harvesting and wastewater recycling, signal a broader shift toward circular resource management.

CtrlS Datacenters has recycled approximately 10 million liters of water, demonstrating the transition from linear to circular water use via wastewater recycling and reuse systems.

Water Management Metrics

Metric | Value / Benchmark | Research Interpretation / Constraint |

| Typical water consumption (1 MW facility) | Up to ~25 million litres per year | Reflects reliance on evaporative and hybrid cooling systems; water demand scales non-linearly with higher rack densities |

| Water Usage Effectiveness (WUE) target (IGBC) | < 2.2 litres per kWh | Serves as a benchmark for water-efficient data centre design; increasingly referenced in green certification frameworks |

| Water recycled (case example – CtrlS) | ~10 million litres recycled | Demonstrates transition from linear to circular water use via wastewater recycling and reuse systems |

| Regulatory water assessments | Mandatory in Chennai and Mumbai | Water impact assessments integrated into project approvals due to urban water stress |

| Primary water risk | Urban water scarcity and climate variability | Heightens operational risk in coastal and metro locations without recycling or alternative sourcing |

| Mitigation approaches | Rainwater harvesting, treated sewage water (TSW), closed-loop cooling | Increasingly treated as core infrastructure rather than compliance add-ons |

| Strategic implication | Water efficiency as resilience metric | Facilities with low WUE and recycling capacity show higher long-term operational resilience |

Capital Intensity and Resource Trade-offs

Current estimates indicate that data center development costs range from INR 60 to 70 crore per megawatt, driven by elevated land prices, advanced cooling technologies, power conditioning systems, and infrastructure designed for AI workloads. Differences in inter-state electricity tariffs and renewable energy access also affect site selection and long-term operational costs.

Research Insight: Collectively, these trends suggest that the evolution of India's data center sector is limited more by engineering feasibility, power reliability, and resource efficiency than by demand. Future competitiveness will rely on integrating high-density computing, low-PUE cooling, resilient power systems, and circular water management into scalable facility designs.

Sustainability Performance and the Renewable Transition

The sustainability transition of India's data center sector is now primarily influenced by operational economics and engineering optimisation, rather than regulatory compliance alone. Cooling systems account for approximately 40% of total data center energy consumption, underscoring thermal efficiency as a key factor for reducing both emissions and costs.

Renewable Energy Adoption Timeline

Major operators are shifting from grid-based electricity procurement to vertical integration with renewable energy generation, incorporating on-site solar installations, long-term power purchase agreements (PPAs), and advanced storage technologies. The adoption of battery energy storage systems (BESS), microgrids, and non-diesel backup solutions demonstrates an innovation-led approach to addressing grid reliability challenges.

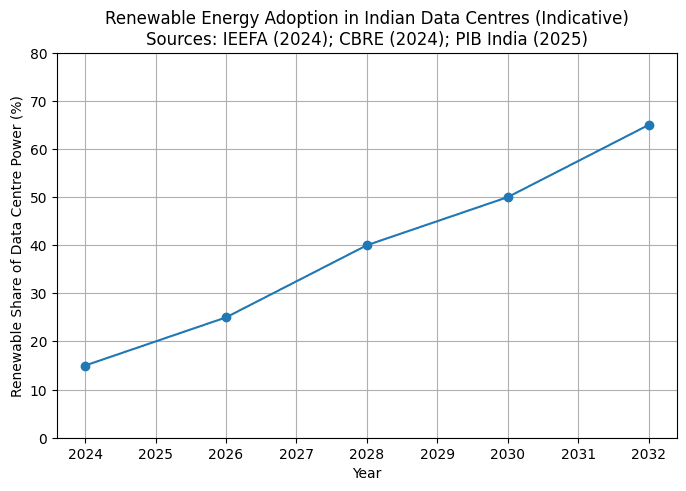

Sector-wide renewable energy penetration is expected to increase from approximately 10–15% currently to around 30% by 2030, supported by fiscal incentives outlined in the Draft National Data Centre Policy (2025). Long-term renewable PPAs provide price stability over 10–20 years, transforming sustainability initiatives from cost centers into strategic hedges against energy price volatility and sources of competitive advantage.

Leading Operator Commitments

Leading operators have publicly committed to achieving 100% renewable energy by 2030, supported by long-term power purchase agreements, on-site solar installations, and grid-scale renewable partnerships. NTT Ltd., Google, and other major players have established renewable energy partnerships to accelerate this transition.

Policy alignment reinforces this shift, as the Draft National Data Centre Policy (2025) proposes fiscal incentives for green-certified facilities, thereby integrating sustainability directly into project economics. Consequently, power sourcing, carbon intensity, and cooling efficiency are now primary design drivers rather than secondary considerations.

Energy Efficiency Benchmarks

Empirical studies indicate that advanced cooling and energy management strategies can achieve significant energy savings and emissions reductions, thereby strengthening the economic rationale for early adoption. Sustainability certifications and industry benchmarks increasingly align with integrated cooling design approaches.

Policy Implications for Energy Transition

Several policy priorities have emerged to support India's data center energy transition:

- Prioritise firm power delivery over capacity creation. As renewable availability is no longer the primary constraint, factors such as grid evacuation, storage, and round-the-clock (RTC) products now drive adoption speed.

- Establish clear frameworks for long-term contracting, including 15–25 year power purchase agreements (PPAs), green open access, and interstate power procurement, to ensure investment certainty for hyperscale data centers.

- Prioritise battery and hybrid renewable energy tenders in states with high concentrations of data centers to enhance 24×7 power reliability.

- Standardise state-level policies by harmonising power tariffs, banking regulations, and renewable energy access across states to minimise execution risk and prevent geographic concentration.

- Integrate sustainability criteria into project approvals by incentivising renewable energy-backed and water-efficient designs, thereby aligning infrastructure development with environmental, social, and governance (ESG) objectives.

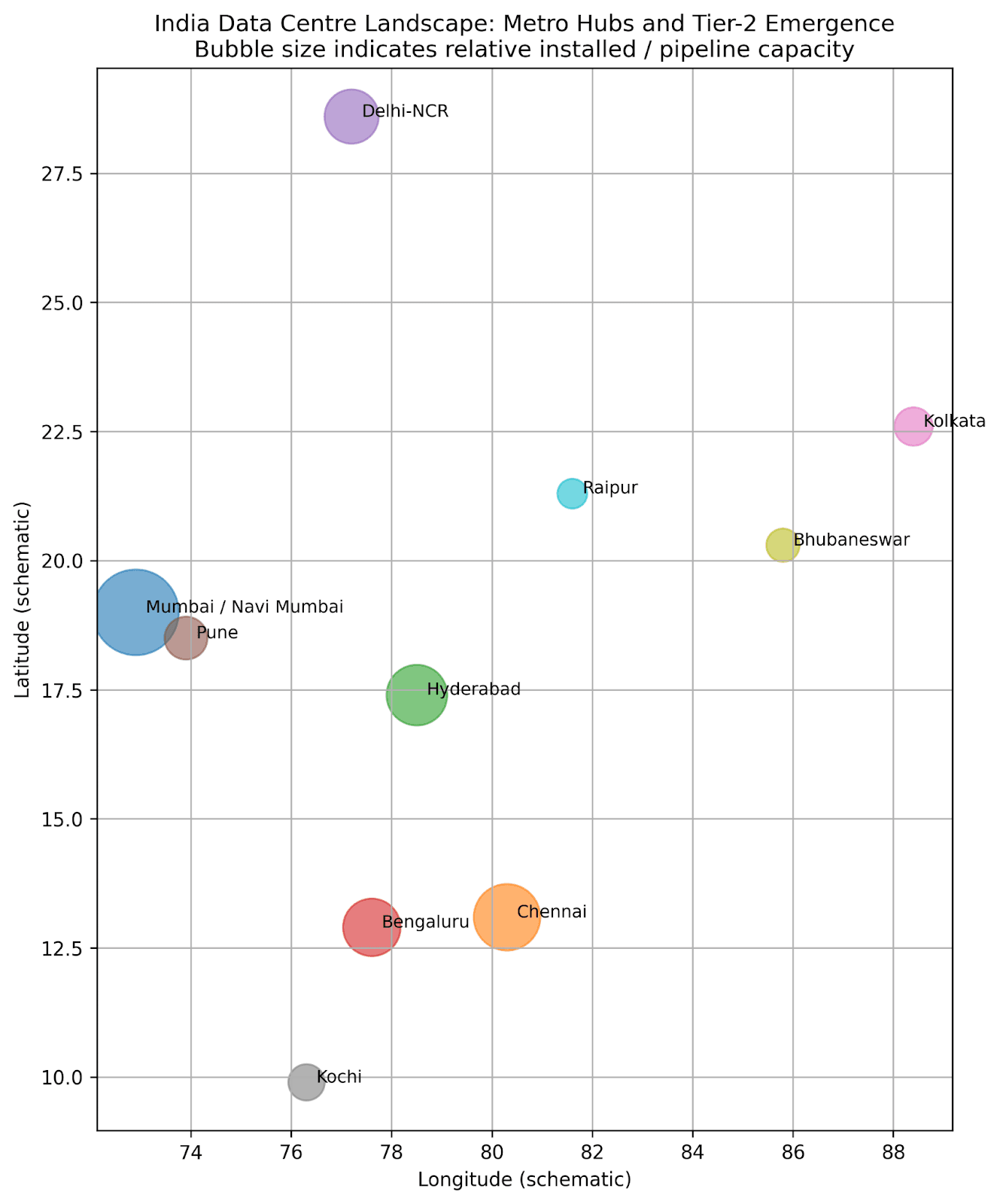

Geographic Distribution and the Tier-2 Emergence

India's data center capacity is primarily concentrated in Tier-1 metropolitan areas due to robust connectivity and high enterprise demand. In contrast, Tier-2 cities are increasingly serving as cost-efficient nodes for edge computing, inference, and resilience, indicating a transition toward a distributed hub-and-spoke infrastructure model.

Cities like Pune, Jaipur, Kochi, Bhubaneswar, and Noida are emerging as strategic locations, offering lower land costs, faster approvals, proximity to regional demand, and growing state-level incentives. This geographic diversification reduces concentration risk while supporting the deployment of latency-sensitive applications closer to end users.

Competitive Dynamics and Market Structure

The data center ecosystem in India is evolving from initial consolidation to gradual diversification. Equipment and cooling markets remain moderately fragmented, with global suppliers establishing performance standards and domestic manufacturers competing on cost and localisation.

Hyperscale operators are increasingly developing self-built, custom-specified facilities, especially for AI workloads, thereby raising the technical requirements for colocation partners. Domestic operators are expanding rapidly, driven by higher utilisation rates and increased demand for AI applications.

International infrastructure providers leverage global operating standards and access to capital to target enterprise and hyperscale clients. The rise of AI-focused investments, such as GPU-centric procurement and regional AI infrastructure, indicates a transition from generic colocation services to compute-intensive platforms.

Overall, the market structure is shifting from a concentrated oligopoly to a more competitive landscape, increasingly favoring participants with reliable power access, advanced engineering capabilities, and integrated sustainability practices.